Lobster industry was a nautical gold rush. Two generations ago, the entire New England coast had a thriving lobster industry.

Today, lobster catches have collapsed in southern New England, and the only state with a significant harvest is north in Maine, where the seafood practically synonymous with the state has exploded.

Now lobsters keep running to the north and going deeper in the water. Maine might be in trouble after another 5-15 years.

Rising temperatures along the bottom of the Atlantic Ocean will force American lobsters (H. americanus) farther offshore and into more northern waters, a new study finds. Credit: Natalie Renier, Woods Hole Oceanographic Institution

That’s happening not only to lobster, but literally to all marine species.

In the U.S. North Atlantic, fisheries data show that at least 85 percent of the nearly 70 federally tracked species have shifted north or deeper, or both, in recent years when compared to the norm over the past half-century. And the most dramatic of species shifts have occurred in the last 10 or 15 years.

Summer flounder’s center of species | Source: NOOA/Oceanadapt, Rugster U., Reuters

Similar findings in a map of predicted migration – marine species are moving northward to colder waters.

Starbucks posted a stellar earnings result today, with net revenue at record level of $6.3bn, beating expectations in many aspects.

Starbucks up after hours with earnings beats | Source: CNBC

While a single beat doesn’t indicate a new stage of growth, in the long run there are three issues I think matter the most and should be watched closely.

1 | Problem: Frappuccino’s decline

It was an problem Starbucks facing over the years. People are leaning towards healthier products (at least a very obvious trend in Cali), which usually means less sugar and less calories. That’s a problem for Starbucks’ Frappuccino, as explicitly mentioned in CEO’s presentation in June.

How did/will Starbucks address this? Product Mix & Innovation

Strategy a) Big push for healthier product lines – Nitro Cold Brew & Refresher series etc.

Starbucks Nitro Cold Brew | Source: Starbucks

– Nitro Cold Brew “is expected to be available in nearly 1,500 stores in 26 markets by the end of 2017″ (SBUX Jul. 2017 Press Release) -> “[Starbucks is] accelerating this platform to more than 2,800 stores by the close of fiscal year 2018, up to more than 6,000 stores by year-end fiscal year 2019″ (SBUX Q3 Earnings Call Transcript). A 4x availability expansion for cold brew in 3 years.

– Several new products in the Refresher category were introduced, e.g. “Dragonfruit” introduced Jun. 2018, “Pink Drink” introduced last year, etc.

Dragon Fruit | Source: StarbucksPink Drink | Source: Starbucks

Strategy b) Instagramable & limited edition within the Frappuccino category

– Unicorn Frappuccino (Apr. 19-23, 2017), Zombie Frappuccino (Oct. 26-31, 2017), Christmas Tree Frappuccino (Dec. 7 – 11, 2017), Crystal Ball Frappuccino (Mar. 22-26, 2018), Witch’s Brew Frappuccino (starting Oct. 25 for a limited time while supplies last)… among many others.

– Plus, Starbucks’ new Frappucino recipe has fewer calories and less sugar, part of its efforts to reduce sugar by 25% by 2020.

Starbucks Rewards could serve a similar role as Amazon Prime. In past last 3 month, loyalty program accounts for 14% of all transactions and US loyalty members contributed 40% of US sales. That’s what happened in the Amazon case, where its Prime members out-spend non-members significantly.

Digital relationship makes it easier to incentivize purchases, market new products/initiatives, bring in more collaborations (e.g. Spotify, Pokémon GO), expand membership offerings and more.

Starbuck’s push for afternoon consumptions is also facilitated by the digitalized promotions.

The room to grow digital relationships is still large – currently 15.3 million global active members, only representing ~22% of its 70 million global customers base. “Additionally, drive-thru, out-the-window and Mobile Order and Pay combined grew to more than 50% of the way customers are ordering, up more than 10 percentage points in just two years” according to COO.

3 | Opportunity – China Growth

It’s more debatable on Starbucks’ China future. Just want to highlight a few sure things.

Starbucks took full ownership in China East & opened flagship Roastery in Shanghai in 2017 – definitely the right moves here.

China’s coffee consumption will explode, even considering major cities alone. Younger generations will consume more coffee and they will represent an increasing proportion of the overall urban population.

China coffee consumption potential | Source: Starbucks 6/19 Presentation

Coffee even has a role to play in China’s GDP growth by boosting workers’ average productivity and the “culture” of working overtime.

Herding effect is stronger in China and “Instagramable & Limited” strategy may provide better outcomes if properly implemented.

Other things worth noticing – Starbucks’ food, packaged goods with Nestlé, next-generation store design, coffee supplies, SKU outside the Starbucks’ core products, etc…

Social network platforms such as Twitter and Weibo, are where we post our words/expressions, and is taking an essential role in todays’ Modern Communication.

Interestingly, but not surprisingly, they are also providing a feedback loop to change our ways of communication (and our thinking – but that’s another different story). After all, we are one of those animals with natural herding inclinations.

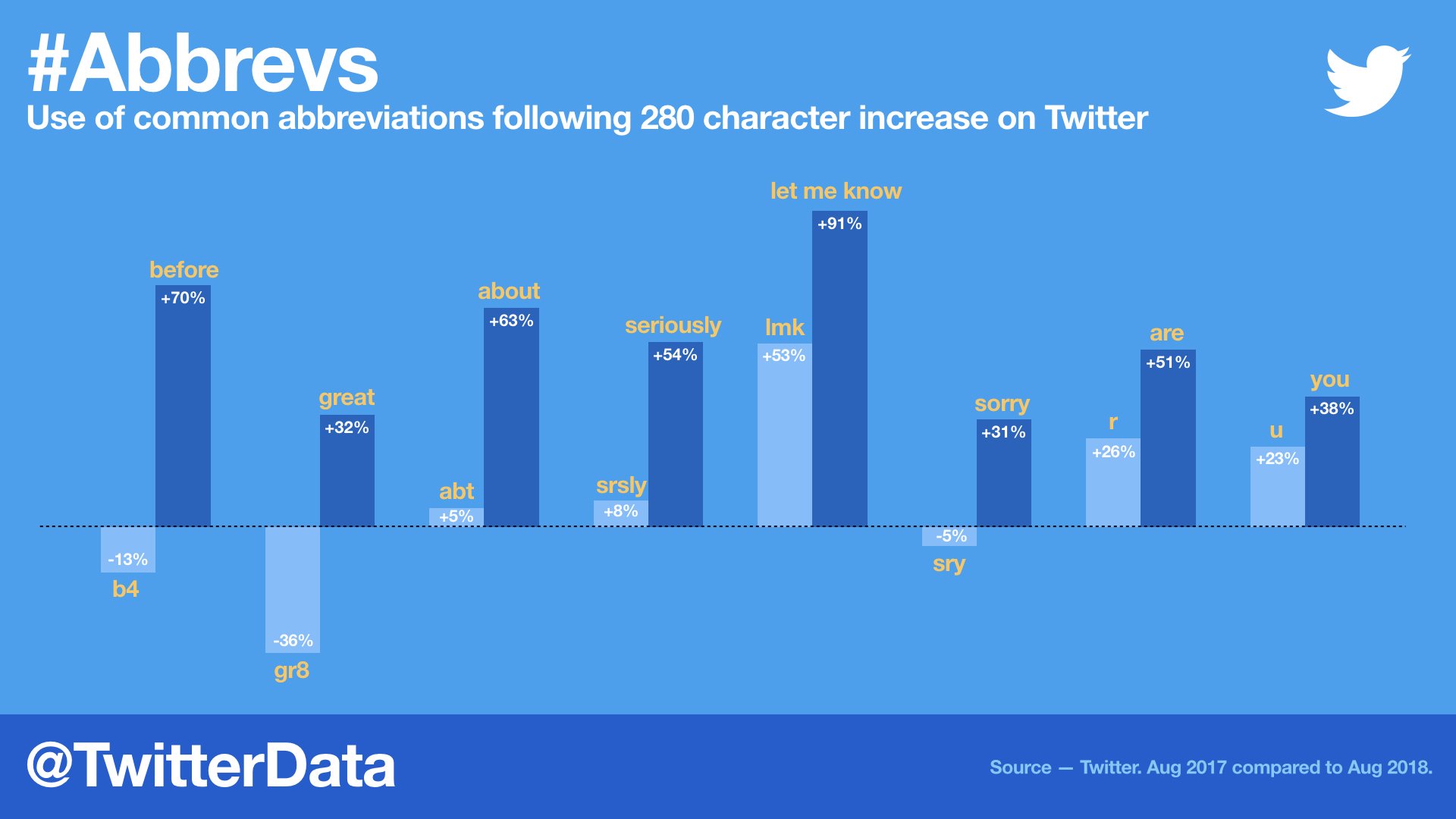

Taking a very simple example – as Twitter was becoming more popular, people started to lean heavily towards the use of new abbreviations, partially due to its 140-word limit. (Similarly, when Blackberries were popular, certain abbreviations were created, used and spread among professionals in texts & emails)

In 2017, Twitter officially made its “140-word limit” a history [Weibo ended the limit in 2016] and doubled the character limit to 280. One resulting impact is that people are spelling out abbreviations and acronyms more often, according to Twitter’s report.

Source: TwitterData

TwitterData also touted that “people are saying ‘please’ (+54%) and ‘thank you’ (+22%) more.” in the first year of doubling limit.

[Something worth noting on the data – 1) need to consider the difference in total number of tweets 2) need to consider other ways of saying ‘please’ and ‘thank you’…]

It is really nice that people could be more friendly and polite (not excessively tho). It would be even nicer if people could inherit their concise and efficient use of language in the 140-word era & all the other positive impacts Modern Communication made on us.

Today Apple announced new products of three lines of business – MacBook Air, iPad Pro and Mac mini.

MacBook Air 2018 Gold | Source: AppleiPad Pro 2018 11-inch and 12.9-inch | Source: AppleMac mini 2018 | Source: Apple

Besides the new features and superior performance, Apple seems to be more addicted to aggressive price tags. Today’s event is the latest episode of a series, starting from the 10-year anniversary model iPhone X last year.

[discussion below is based on the most basic consumer version of each product]

9/12/2017 – iPhone X introduced @ $999, a 30% increase from the high-end phone (iPhone 7 Plus @ $769) one year before

5/27/2018 – updated iPad introduced @ $329, flat with the new iPad debut price in Apr. 2017.

7/12/2018 – updated MacBook Pro @ $1,799; the price seems to be the same as Oct. 2016’s debut price with Touch Bar, but is a 20% increase in terms of available low-end option (MacBook Pro with no Touch Bar @ $1,499).

9/12/2018 – iPhone XR @ $749, increased by 7% ($50) compared to the low-end phone last year (iPhone 8 @$699) ; Apple Watch Series 4 @ $399, increased by 21% ($70) from a year ago @ $329.

10/30/2018 – new MacBook Air @ $1,199, a 20% increase from the old model years ago @ $999; updated iPad Pro @ $799, a 23% ($150) increase from previous Jun. 2017 version @ $649; new Mac mini @ $799, a 60% increase from the old model years ago @ $499; redesigned Apple Pencil 2 @ $129, increased by 30% from $99 when it was introduced 3 years ago

The 2-way strategy looks clear: 1. use entry-level new products (e.g. iPad & iPhone XR) to attract new users and compete with other firm’s often lower-priced products. Educational market and some international markets are important here, especially for new-user growth, ensuring an increasing number of total active users in Apple’s ecosystem and getting more market shares in terms of shipment. So there is barely any increase in price. 2. raise prices by 20-30% in other product lines to keep margin (for example Apple Watch price increase might be more associated with costs) or to compensate lower margins in entry-level products.

Apple’s overall average gross margin from 2016 to present is actually lower than the average from 2014 to 2015 (38.44% vs. 39.63%, down ~120bp), even with higher gross margins from service revenues weighing in more recently.

1. How big is today’s loss & Are we really panicking?

The market rout on 10/24 (NASDAQ Composite dropped 329.14 points to 7,108.40) made it the largest retreat so far this year, surpassing the previous 316-points loss merely 2 weeks ago (10/10).

US stock index 10/24 tumble | Source: WSJ, Dow Jones Market Data

While the 4.43% retreat is widely “touted” as the biggest one-day loss since August 2011, it’s also the 3rd largest daily point loss in NASDAQ history (the other two happened in 2000 during the dot-com bubble).

Top 10 NASDAQ Largest Point Decrease as of 10/24/2018

However, in percentage wise, we could see NASDAQ’s 10 biggest single day decrease ranging from -11.35% to -7.23% (3 of which related to the 2008 financial crisis, 3 related to the dot-com crash, another 3 related to the 1987 crash).

“-4.43%” is not a big deal & that’s not how investors react if they are really panicking.

2. All about inflation?

It’s crucial to incorporate inflation into analysis.

NASDAQ climbed above 5,000 in Mar. 2015, and it took another 7 weeks before it reached the dot-com bubble peak of 5048.61 (intra-day record was 5,132.52).

NASDAQ Composite climbed above 5,000 in Mar. 2015 | Source: Quartz, FactSet

However, when we adjust for inflation, things are different.

Doing a simple math – U.S. CPI (urban, all items ex. food & energy) is 181.3 in 2000 (annual average) and 256.5 in 2018 (H1 average); so a 8,109.69 peak in August should be around 5,732 in 2000-price-level.

So NASDAQ Composite spent more than 18 years to grow 13.5% (from peak to peak), while fundamentally technology has gone through tremendous evolutions.

CPI – urban consumers, ex. food & energy (Jan. 1999 – Sep. 2018) | Source: U.S. Bureau of Labor Statistics

Similarly, WSJ reported in January this year that “Nasdaq Tops Inflation-Adjusted High [7269.89] from Dot-Com Boom”; and the chart below shows the inflation-adjusted path.

Why did we wait for 18 years just for a come-back? So value creation has little to do with the price? Is this all about inflation in the end?

3. Sit back and relax – It’s NOT all in vain

It’s a sure thing that companies can be over- or undervalued over time. But the benefits and growths are also real.

We have (unprecedented) iPhone in 2007 and (finally) massively produced Tesla Model 3 in 2018; we have 1 TB cloud storage for $9.99/month on Dropbox/Google Drive and unlimited storage of business account for $15/month on Box or $10/month on OneDrive.

Development in biotech is equally impressive. Sequencing cost dropped from ~$100 million per genome in early 2000s to ~$1,000 in 2016; and we are curing/curbing more types of cancer with unprecedented success rate and less harmful methods. Other advancements, for example those in neuroscience or surgical robots, are no less exciting.

And we can see their reflections in stock price (e.g. AAPL TSLA ILMN ISRG).

While the NASDAQ Composite in 2000s may be overvalued, comparatively in 2018 it is more supported by concrete revenue and earnings. Promises and expectations are still built in the price, but things are a lot better.

From a similar discussion in Mar. 2015 when NASDAQ reached 5,000 again after 15 years – P/E is not even close to insane levels.

When we call it a bubble (e.g. dot-com bubble), it is usually characterized by an increasing [absurdly large] difference between price and actual value created.

Revenue or earnings can rarely be doubled consecutively between regular quarters but prices can. That’s what happened in 1999 when Nasdaq Composite rose 85.59% (vs. 28.24% in 2017) and 13 large-cap stocks rose over 1000% (vs. Amazon +56%, Netflix +55%, Facebook +53%, Apple +46%, Alphabet +33% in 2017).

While a 10-fold rise in stock price is tough to catch up by revenues and earnings, I see a 50% rise doable and reasonable (e.g. could be a combination of 80% EPS growth + 20% P/E decrease, 50% EPS growth + P/E unchanged, or 25% EPS growth + 20% P/E increase), as long as the new P/E is justified by the future prospect.

I am not saying we shouldn’t anticipate a correction; but NASDAQ Composite hasn’t been super crazy neither.

I would like to conclude this post here by saying that – I believe in the future and the real benefits of tech [if correctly used]. Some areas might seem to be more over-promised than others, and some risks are looming on the horizon [to negatively impact global economy in a nontrivial manner], but true value creation should and will always be valued.

Appendix – what does S&P look like

S&P forward P/E as of Sep. 2018 | Source: JP Morgan Asset Management

Google 肯定是要抢这个未来 smart home device 核心位置的,nest 已布局多年,推广 google assistant(智能语音),顺带连接 google 本身各项服务,以及推广 youtube (premium) music。Google 的硬件实力近几年也突飞猛进,系统平台的强势更不用说。

Microsoft 这个略尴尬,也不算它自己做的 device,主要是推广了 Microsoft 的 Cortana 智能语音。

Apple 不用说,音乐和硬件一直是强项,Siri 也是有基础的,iOS 本身也有 Homekit。虽然目前没有带屏幕,但我相信就是日程上的事。已经有 FaceTime 和 FaceID,想象空间绝对够。

Facebook 强在社交网络 (FB Messenger) 的嫁接,自动生成电话薄。

然而,Facebook Portal 细想一下,在很多方面都很尴尬。

首先,Facebook 没有自己的智能语音,Portal 是直接用的 Amazon Alexa。在这一群科技巨头面前直接弱三分 (Alexa, Google Assistant, Cortana, Siri)。

Banksy B. 1974 GIRL WITH BALLOON signed and dedicated on the reverse spray paint and acrylic on canvas, mounted on board, in artist’s frame 101 by 78 by 18 cm. 39 3/4 by 30 3/4 by 7 in. Executed in 2006, this work is unique.BANKSY, LOVE IS IN THE BIN, 2018

作者 Banksy 在 Instagram 上 po 出了自带碎纸的画框制作小视频,并 quota 毕加索

“The urge to destroy is also a creative urge” – Picasso

原本约 1 百万英镑的拍卖成交价,在一波戏剧性的操作后作品将大幅增值。

虽说 Banksy 说拍卖行并无参与 – 但无论怎样,这已经不单单是一幅画作,整个戏剧性故事都离不开 Sotheby。根据苏富比的 blog,这是首次在拍卖中卖出了行为艺术 (it marked the first time a piece of live performance art had been sold at auction, read more here)。

提案方包括 Trillium Asset Management (53,000 shares),以及纽约市 Comptroller 和三个州的 State Treasurer – Illinois (190,712 shares) , Rhode Island (168,230 shares) and Pennsylvania (38,737 shares), New York City Pension Funds (4.5 million shares),大约近 500 万股(占 0.2%)。